Check if you need to tell the government about an acquisition that could harm the UK's national security

Investors and businesses may be legally required to tell the government about certain sensitive acquisitions under the National Security and Investment Act.

The government can scrutinise and intervene in certain acquisitions that could harm the UK’s national security. They can impose certain conditions on an acquisition and in rare cases may unwind or block an acquisition completely.

The rules apply to acquisitions that are in progress, contemplation or have been contemplated. Acquisitions completed before 12 November 2020 are exempt.

If you are planning an acquisition of a qualifying entity in one of 17 defined sensitive areas of the UK economy, you may need to get approval from the government before you can complete it. This is called a notifiable acquisition. Completing a notifiable acquisition without approval will mean the acquisition is void and may mean that the acquirer is subject to civil or criminal penalties.

This guidance tells you:

- what types of acquisitions are covered

- when you need to tell the government about an acquisition

- how the government will scrutinise the acquisition

These rules fall under the National Security and Investment (NSI), which came into force on 4 January 2022. The Act is administered by the Investment Security Unit (ISU) in the Department for Business, Energy and Industrial Strategy (BEIS) and the decision maker is the Secretary of State for BEIS.

How the rules work

-

Check if the rules apply to your acquisition. This will depend on what you are acquiring and how much control you have over it.

-

Check if you need to tell the government about your acquisition. You are legally required to inform the government about certain acquisitions of entities if your acquisition is in a sensitive area of the UK economy.

-

Tell the government about your acquisition. You can do this online by submitting a notification using the National Security and Investment service.

-

The government will review your acquisition. It can either clear your acquisition, impose certain conditions, or block or unwind it.

Check if the rules apply to your acquisition

The new rules only apply to qualifying acquisitions. These are referred to as trigger events in the National Security and Investment Act.

Your acquisition is a qualifying acquisition if all of the following apply:

- the acquisition is of a right or interest in, or in relation to, a qualifying asset or qualifying entity (these terms are explained below)

- the entity or asset you are acquiring is from, in, or has a connection to the UK

- the level of control you acquire over the qualifying entity or qualifying asset meets or passes a certain threshold (for example, your stake or voting rights in a qualifying entity becomes higher than 25%)

- the acquisition was not completed before 12 November 2020

If the government reasonably suspects that an acquisition meets these criteria and that it has given rise to, or may give rise to, a risk to national security, it can be scrutinised by the government.

In addition, if this qualifying acquisition is of an entity in one of the 17 defined sensitive areas of the economy it may need to be notified to the government. Qualifying acquisitions outside the 17 defined areas do not need to be notified to the government.

Check if you are acquiring a qualifying entity or asset

A qualifying entity is any entity other than an individual, including:

- a company

- a limited liability partnership

- any other body corporate

- a partnership

- an unincorporated association

- a trust

Qualifying assets include:

- land

- tangible moveable property

- ideas, information or techniques which have industrial, commercial or other economic value (‘intellectual property’)

Entities and assets might be qualifying entities and qualifying assets if they are outside or not from the UK but have a connection to the UK.

Acquisitions of entities or assets outside or not from the UK

If an entity is formed or recognised under the law of a country or territory outside the UK, it is a qualifying entity if it either:

- carries on activities in the UK or

- supplies goods or services to people in the UK

For land or tangible moveable property situated outside the UK or its territorial sea, or for any intellectual property, it is a qualifying asset if it is either:

- used in connection with activities carried on in the UK or

- used in connection with the supply of goods or services to people in the UK

Read further guidance on how the rules work for entities and assets outside or not from the UK.

Check the level of control you have acquired, or will acquire, over the qualifying entity or asset

If you are acquiring a qualifying entity or asset that is from, in, or has a connection to the UK, you will need to check if the level of control you have acquired, or will acquire, over it could bring it in scope of the rules.

Your acquisition is in scope of the rules if you acquire a right or interest in, or in relation to, a qualifying entity or asset, and the level of control you acquire meets any of the following thresholds:

- your shareholding stake or voting rights in a qualifying entity meets or crosses certain percentage thresholds (for example, it becomes higher than 25%)

- you acquire voting rights in a qualifying entity that allow you to pass or block resolutions governing the affairs of the entity

- you are able to materially influence the policy of a qualifying entity, for example acquiring the right to appoint members of the board of the entity that enables you to influence the strategic direction of the entity

- you are able to use a qualifying asset, or direct or control its use, or you are able to do so more than you could prior to the acquisition

If your qualifying acquisition takes place over more than 1 day, the acquisition will be treated as having taken place on the last day of the period.

Further details of each threshold are outlined below.

If your shareholding stake or voting rights meet or cross certain percentage thresholds

Your acquisition is in scope if your shareholding stake or voting rights increase:

- from 25% or less to more than 25%

- from 50% or less to more than 50%

- from less than 75% to 75% or more

If the entity has a share capital, the thresholds describe holding shares comprised in the issued share capital of a nominal value (in aggregate) of that percentage of the share capital.

If the entity does not have a share capital, the thresholds describe holding a right to that percentage share of the capital or profits of the entity.

If the entity is a limited liability partnership, the thresholds describe holding a right to that percentage share of any surplus assets of the partnership on its winding up. Where this is not expressly provided for, each member will be treated as having an equal share.

Example

Investor A owns 20% of Entity B and acquires shares comprising 10% more, leaving Investor A with 30% in total. This is a qualifying acquisition because it takes Investor A’s shareholding from 25% or less to more than 25%, which is a qualifying acquisition threshold set out in the NSI Act.

Investor A then acquires an additional 10%, leaving them with 40% of the shares. This is not a qualifying acquisition because Investor A’s shareholding has not met or passed any of the 3 thresholds.

Investor A then acquires an additional 15%, leaving them with 55% of the shares. This is a qualifying acquisition because it takes Investor A’s shareholding from 50% or less to more than 50%, which is a qualifying acquisition threshold.

If you acquire voting rights that allow you to pass or block resolutions governing the affairs of the entity

Such an acquisition is in scope of the rules, regardless of the percentage of voting rights you may already hold, or the percentage of your shareholding, or taking into account other voting rights you hold as well as your acquisition. Any voting rights you already held before the acquisition are taken into account when assessing whether the acquisition meets this threshold.

Voting rights means rights that are given to shareholders or members to vote at general meetings on all, or substantially all, matters.

If the entity does not have general meetings at which matters are decided by such votes, voting rights includes any rights in relation to the entity that are of the equivalent effect.

In the case of minority veto rights, the voting rights only count where they provide the holder with a right to vote on all or substantially all matters governing the affairs of the entity.

Example

Person A owns 20% of an entity’s voting rights and acquires a preferential share which provides them with the ability to pass, by themselves, ordinary resolutions. This is a qualifying acquisition because the acquisition gives Person A the ability to pass resolutions governing the affairs of the entity.

If you acquire a right or interest in, or in relation to, a qualifying entity which provides you with ‘material influence’ over the entity’s policy

The Competition and Markets Authority has produced guidance on its assessment of material influence when operating the merger control regime under the Enterprise Act 2002.

When making its assessment, the CMA focuses on the acquirer’s ability materially to influence policy relevant to the behaviour of the target entity in the marketplace. The policy of the target in this context means the management of its business, and thus includes the strategic direction of a company and its ability to define and achieve its commercial objectives. Any assessment by the government of an acquisition of material influence under the NSI Act will be considered in the light of the relevant section on material influence in the CMA guidance but applying the concept in the context of the NSI Act, so far as is appropriate.

The material influence threshold in the NSI Act does not apply if:

- you are acquiring an asset

- you already hold a right or interest enabling you to materially influence the policy of the entity

Example

Investor A acquires a 20% shareholding in Entity B, and, in this instance, this makes Investor A the largest single shareholder of the entity. Taking into account Investor A’s status and expertise in the sector and resulting influence over the actions of other shareholders, Investor A may be judged to have acquired material influence over the entity and, in such circumstances, this would be a qualifying acquisition.

If you acquire a right or interest in, or in relation to, a qualifying asset and as a result you are able to use, or to direct or control how the asset is used, or can do so to a greater extent than before the acquisition

This could include acquiring a right or interest that gives you the ability to use, or to direct or control the use of an asset, even if you do not acquire the asset itself.

Qualifying assets include land, tangible moveable property and intellectual property, and these may be within or outside the UK. If an asset is outside the UK, or is intellectual property, it must have a sufficient connection to the UK. Read further guidance on how the new rules will work for entities and assets outside or not from the UK.

Example

Company A’s sole business is to manufacture equipment. Party B operates in a similar area for a range of clients. Party B does not acquire Company A but does acquire its equipment.

This is a qualifying acquisition because Party B acquires the assets and as a result can use or direct or control the use of these assets. If Party B signed a contract with Party A providing it with rights to use the assets, that would also be a qualifying acquisition.

IfInternal yourcorporate qualifyingreorganisations

Entities acquisitioncarry isout internal reorganisations for a range of reasons, including seeking to simplify the corporate structure, reduce compliance costs and reporting complexity, preparing part of a corporategroup restructurefor orsale, reorganisationand overall business rationalisation.

QualifyingThe government considers that internal reorganisations can be qualifying acquisitions where they result in an acquisition of control over a qualifying entity (as defined in Section 8 of the NSI Act), even if the ultimate beneficial owner of the entity remains the same.

Additionally, the acquisition may be subject to mandatory notification if it meets the relevant tests in the NSI Act.

The government recognises that aremost partacquisitions of this kind will simply be a product of internal corporate restructurerestructuring orand reorganisationefficiency.

There may be coveredrare bycases where the rules.acquisition Thisof iscontrol over an entity by a person in the casesame business group raises national security risks. That may be true even if the acquisitionultimate takesbeneficial placeowner withinis the same before and after the qualifying acquisition.

This is because an acquisition of control by another “link” in the corporate group.structure – particularly one where the ultimate beneficial owner is passive – could enable a hostile actor to pursue malign actions over the entity.

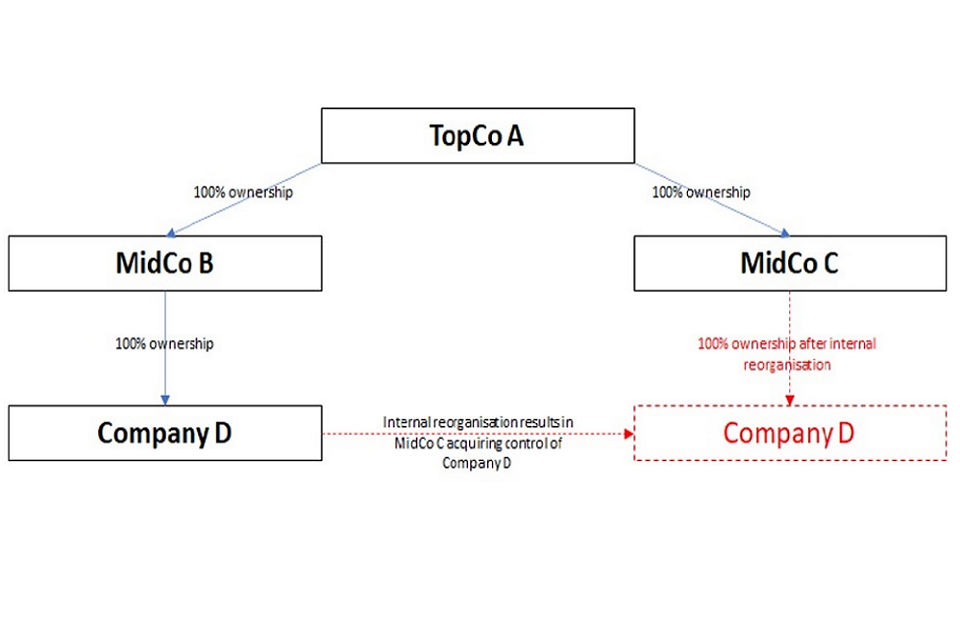

This meansdiagram is an example of an internal reorganisation:

In this example the internal reorganisation involves the transfer of MidCo B’s 100% shareholding and voting rights in Company D to MidCo C.

While the ultimate beneficial owner, TopCo A is the same before and after the internal reorganisation – and their level of their indirect holding in Company D remains unchanged – this does not negate that evenMidCo withinC corporateis restructures,acquiring control over Company D. This therefore constitutes a qualifying acquisition.

If Company D carries on activities in the UK that are specified in Notifiable Acquisition Regulations, this also requires mandatory notification. MidCo C must therefore notify the Secretary of State of the proposed acquisition and receive clearance before it can take place.

The appointment of liquidators or other insolvency measures

The appointment of liquidators and receivers may constitute a qualifying acquisition under the NSI Act and, in some specific scenarios, may require mandatory notification.

Schedule 1 to the NSI Act does not treat rights that are exercisable by an administrator or by creditors while an entity is in relevant insolvency proceedings as being held by the administrator or creditors. This approach does not, however, include rights held by liquidators or receivers, who may oversee the winding up of an entity or the enforcement of secured assets – an action that could, in certain situations, raise national security risks.

This means the appointment of a liquidator or receiver may be a qualifying acquisition, and in specific cases may require mandatory notification. This will depend on whether and how the circumstances of the appointment meet the requirements of the NSI Act.

There are 2 scenarios, set out below, where the appointment of a liquidator or a receiver may result in them holding a right or interest in another entity. Their appointment may then require mandatory notification if the notifiable acquisition criteria are met.

Scenario 1

The liquidated entity has shares in a solvent entity. During the insolvency process, and prior to notify.these shares being sold, the liquidator or receiver has voting rights over these shares. This is an acquisition of control and, if relevant tests are met – including if the solvent entity carries on activities specified in the notifiable acquisition regulations – could require mandatory notification.

Scenario 2

An individual, such as a director, is declared bankrupt and holds shares in a solvent entity. These shares are transferred over to the trustee in bankruptcy during the insolvency process. This is an acquisition of control and, if relevant tests are met – including if the solvent entity carries on activities specified in the notifiable acquisition regulations – could require mandatory notification.

When these scenarios occur and parties need to submit a mandatory notification, such notifications are subject to the same timelines as other notifications.

Indirect acquisitions of control

Under the NSI Act, it is possible for investors and other parties to acquire control over qualifying entities indirectly. This happens when there is an unbroken chain of majority stakes down to an entity of interest.

Schedule 1 in the NSI Act defines 4 types of majority stakes:

a) Company A holds a majority of voting rights in Company B; or

b) Company A is a member of Company B and has the right to appoint or remove a majority of the board of directors of B; or

c) Company A is a member of Company B and controls alone, pursuant to an agreement with other shareholders or members, a majority of the voting rights in Company B; or

d) Company A has the right to exercise, or actually exercises, dominant influence or control over Company B.

Example 1

TwoCompany partiesA shareacquires 51% of the sameshares ultimatein ownerCompany B, which in turn already holds 51% of the shares of Company C.

Company A has not only acquired direct control over Company B, but areit runhas separatelyalso fromacquired eachindirect other.control Oneover Company C, and the rules in the NSI Act apply as if Company A was acquiring shares directly in Company C. This means that, assuming the other relevant tests in the NSI Act were met, Company A has made two qualifying acquisitions – the direct acquisition of Company B and the partiesindirect acquisition of Company C.

If, instead, Company A had not acquired a majority stake in Company B (and none of (b) – (d) above were satisfied), or Company B did not have control (within section 8(1)) over Company C, Company A would not have acquired indirect control over Company C.

Example 2

Company A acquires part51% of shares in Company B, which in turn already holds 51% of shares of Company C, which in turn owns 26% of shares in Company D. Company D carries on activities specified in the otherNotifiable Acquisition Regulations, but Companies B and C do not.

Through the chain of majority stakes, Company A has indirectly acquired control in Company D. Because Company D carries on activities specified in the Notifiable Acquisition Regulations, this is a notifiable acquisition, meaning it must be notified and receive clearance from the government before it can be completed. Further guidance on notifiable acquisitions. In addition, Company A has also acquired direct control over Company B and indirect control over Company C, both of which may also be qualifying acquisitions (meaning they can be voluntarily notified and called in for scrutiny, even if they are not subject to mandatory notification requirements) if the relevant tests in the NSI Act are met.

If an indirect acquisition means that an acquirer has made more than one qualifying acquisition at the same time then a single notification may be sufficient. Parties in this situation should read this section: When you can submit a single notification for multiple acquisitions.

The granting of security over shares

The granting of share security occurs where a person who owns shares in a qualifying entity (the borrower) grants security over those shares in favour of another person (the lender or a security trustee on behalf of a number of lenders). It is typical for the lender and borrower to agree that if a certain event takes itsplace (for example, a default on the loan), the lender or security trustee will be able to enforce the share security and gain control over onethe share, allowing them to exercise voting rights in respect of the thresholdsshares. The granting of share security is separate from the enforcement of that share security, which may or may not occur at a further point in time.

The granting of types of share security where title to makethe shares is not transferred to the secured lender (or its nominee) is not a notifiable acquisition requiring mandatory notification, even if it involves an entity carrying on activities covered in the Notifiable Acquisition Regulations.

The NSI Act concerns relevant acquisitions of control. Sections 8(2), 8(5), and 8(6) set out some of the ways that an acquirer might acquire control over an entity. If an acquirer gains control, under those sections, over an entity carrying on particularly sensitive activities set out in the Notifiable Acquisition Regulations, that will require mandatory notification and clearance before the acquisition can be completed. These sections set out the following ways to gain control:

- the acquirer’s shareholding stake or voting rights in a qualifying

acquisition.entity meets or crosses certain percentage thresholds – for example, it becomes higher than 25% - the acquirer acquires voting rights in a qualifying entity that allows them to pass or block resolutions governing the affairs of the entity

However, the granting of such share security does not constitute any of these types of acquisitions of control.

Whilst the grant of a security over shares could create an equitable interest in such shares, such an interest would not appear to grant any control over the shares, as referred to in section 8(1) of the NSI Act, until the happening of an event that would provide control.

Section 8(2) of the Act should be read in conjunction with section 8(1) and (3) of the NSI Act. Section 8(1) provides that a person gains control of a qualifying entity if the person acquires a right or interest in, or in relation to, the entity and as a result one of the cases of control set out in section 8 arises.

The ultimatecase ownerset remainsout in section 8(2) relates to an increase in the same,shareholding butof theirthe ownershipperson nowand goessection through8(3) expands on the reference to “holding a differentpercentage corporateshare” chain.in section 8(2). The holding of shares in this context is a reference to having shares in a company. Whilst the grant of a security over shares could create an equitable interest in such shares, such an interest would not appear to grant any control over such shares, as referred to in section 8(1), unless or until an event that would provide control happens. The creation of a share pledge over shares in a qualifying entity of a specified description under Scots law, where title to the shares is transferred to the secured lender or its nominee, would require prior notification and clearance from the government.

Similarly, the case set out in section 8(5) relates to an increase in voting rights that the person holds in the entity. Such an increase in voting rights would also not appear until the event that would provide control happens.

This means thereit is not mandatory to notify and receive clearance from the government before granting equitable share security.

Notwithstanding the above, if legal title is transferred or control passes in some other way, and the shares qualify under the Notifiable Acquisition Regulations, a notifiable acquisition has beentaken place and must be notified to the Secretary of State before completion.

Different types of voting rights and mandatory notification

The NSI Act concerns acquisitions of control over qualifying entities and qualifying assets. In respect of entities, Section 8(6) means that the NSI Act applies to acquisitions of voting rights that enable a changeperson to secure or prevent the passage of any class of resolution governing the affairs of the target entity.

Whilst the thresholds specified in sections 8(2) and 8(5) (i.e. over 25%, over 50% and 75% or more of shareholding or voting rights) have strong relevance in UK company law, companies can still set alternative thresholds, and entities that are not companies have greater flexibility to set alternative thresholds for passing or blocking resolutions (or their equivalent). Section 8(6) applies to these circumstances.

There are circumstances where parties have contractual rights that may have the effect of securing or preventing the passage of a class of resolution. These are frequently taken by minority investors when providing early-stage investment and may occur in other circumstances too.

The government considers that such contractual rights are not covered by the NSI Act under section 8(6) on the basis that such contractual rights are not themselves voting rights as set out in section 8(7), provided such contractual rights do not amount to control of such voting rights under paragraph 5 of Schedule 1.

In addition, such contractual voting rights would need to enable the acquirer to secure or prevent the passage of all resolutions of a particular class to be relevant for the purposes of section 8(6).

Notwithstanding the above, the government recognises that the breadth of matters which might be subject to investor consent is extensive. While minority investors may typically seek strong protections – particularly in the case of early-stage investment – the government is also mindful of those seeking to exert malign influence over sensitive businesses through the use of contractual rights.

That is partly why the NSI Act.Act Thisalso defines control in section 8(8) as an acquisition which enables a person materially to influence the policy of the entity.

It may be, depending on the facts of the case, that contractual rights – either alone or together with other interests or rights – give an acquirer material influence.

Unlike voting rights in section 8(6), an acquisition of material influence is truenot evensubject thoughto mandatory notification. However, the ultimateparties ownermay remainssubmit a voluntary notification. Whether a notification is submitted or not, the same.Secretary of State may call in qualifying acquisitions where they reasonably suspect the acquisition may give rise to a risk to national security.

If you are planning a qualifying acquisition but it has not yet taken place

The government can assess a potential qualifying acquisition that has not yet happened if it reasonably suspects it may cause a national security risk. The government can call in a qualifying acquisition that has already happened, or is in progress or contemplation.

Example

Entity A is negotiating an agreement for the purchase of 100% of UK Company B and has signed heads of terms. This is likely to be interpreted as a qualifying acquisition that is in contemplation. Even though the acquisition has not yet happened, the government may still be able to call it in.

Interests and rights

Interests and rights count as acquired if you begin to hold them in any of the following ways:

- hold an interest or right jointly with someone else

- have a joint arrangement with someone else that means you will exercise all, or substantially all, of the rights or interests in a way pre-determined by the arrangement. The Act has a broad definition of ‘arrangement’ which means most types of arrangement count under these rules

- hold a majority stake in an entity that holds the interest or right, or is part of a chain of entities which each hold majority stakes through the chain and the last one holds the interest or right

- a nominee holds an interest for you

- control a right that is owned by another party (unless the owner also controls the right)

- hold a right exercisable only under certain circumstances, when the circumstances have arisen or you control whether those circumstances exist. This does not apply to administrators or creditors, who are not regarded as holding those rights while an entity is in relevant insolvency proceedings in certain circumstances, hold a right attached to shares which are held as security by a lender. The owner, not the lender, is treated as owning or acquiring the rights where the rights are exercisable only in accordance with the owner’s instructions (apart from exercising the rights for the purpose of preserving the value of the security, or of realising the value). It is also the case where the shares are held in connection with loans as part of normal business activities and the rights are exercisable only in the owner’s interest (apart from exercising the rights for the purpose of preserving the value of the security, or of realising it)

- hold combined rights or interests with another person by virtue of being connected (for example, a spouse or relative or 2 or more undertakings in one group)

- hold rights or interests with another person or more people, with whom you share a common purpose (for example, coordinating influence on an entity’s activities)

Check Schedule 1 of the Act for full details. This includes some specific limitations of what is considered as acquired such as whether an acquisition has taken place when shares are given as security for a loan.

Check if you need to tell the government about your acquisition

You are legally required to tell the government about certain acquisitions of qualifying entities in 17 sensitive areas of the economy subject to certain criteria. These are mandatory notification requirements, known as ‘notifiable acquisitions.’

You must get approval from the government before you complete the acquisition otherwise the acquisition will be void. You can do this by submitting an online form to the government (called a ‘mandatory notification form’).

The government will then review your acquisition to see if it could cause a national security risk. If the government clears the acquisition, it cannot assess it again, unless false or misleading information was submitted.

When you will be legally required to tell the government about your acquisition (mandatory notification)

If you are a party acquiring a qualifying entity, you must tell the government about certain acquisitions in 17 sensitive areas of the economy. These are called ‘mandatory notification’ requirements and cover areas which are considered more likely to give rise to national security risks.

The 17 areas of the economy are:

- Advanced Materials

- Advanced Robotics

- Artificial Intelligence

- Civil Nuclear

- Communications

- Computing Hardware

- Critical Suppliers to Government

- Cryptographic Authentication

- Data Infrastructure

- Defence

- Energy

- Military and Dual-Use

- Quantum Technologies

- Satellite and Space Technologies

- Suppliers to the Emergency Services

- Synthetic Biology

- Transport

You need to tell the government about a notifiable acquisition by submitting a mandatory notification online. Qualifying acquisitions which are subject to mandatory notification requirements are called ‘notifiable acquisitions’.

If you are notifying, you will be asked to provide information on the structure and share ownership of the qualifying entity, the acquirer and the acquisition.

Mandatory notification requirements only apply to the acquisition of qualifying entities. These requirements do not apply to the acquisition of qualifying assets.

Your acquisition is a ‘notifiable acquisition’ if it meets the following criteria:

-

You are acquiring a qualifying entity that carries out certain activities in the UK within one of 17 sensitive areas of the economy.

-

And any of the following apply:

i) Your shareholding stake or voting rights increase:

- from 25% or less to more than 25%

- from 50% or less to more than 50%

- from less than 75% to 75% or more

ii) Your acquisition is of voting rights and this will enable you to secure or prevent the passage of any class of resolution governing the affairs of the entity.

Check if your acquisition is a notifiable acquisition when the entity is outside the UK

For notifiable acquisitions, a qualifying entity falls within the scope of mandatory notification requirements only if it carries out the activity specified in the regulations in the UK.

If a qualifying entity is formed or recognised under the law of a country or territory outside the UK and carries on activities in the UK which are specified in the notifiable acquisition regulations then the acquisition of such an entity may be a notifiable acquisition.

Example

Company A undertakes notifiable acquisition activities in Germany, but also undertakes activities within the UK which are not in scope of the notifiable acquisition regulations. An acquisition of company A would not constitute a notifiable acquisition as it does not undertake the specified activities within the notifiable acquisitions within the UK.

Example

Company B is a US-based company that supplies robotics parts to the UK. It does not undertake any activities within the UK besides supplying parts of the UK. This would not constitute a notifiable acquisition as Company B does not undertake the specified activities in the UK.

If you do not tell the government about a notifiable acquisition

The acquisition is void if you complete a notifiable acquisition without notifying and gaining approval from the government. You will be able to apply for retrospective validation online.

There are civil and criminal penalties for completing a notifiable acquisition without gaining the necessary approval. A civil penalty could require you to pay up to 5% of your organisation’s global turnover or £10 million, whichever is greater.

If you have an acquisition that is not covered by mandatory notification

You are not legally required to tell the government about your qualifying acquisition if it is not covered by a mandatory notification. You can submit a voluntary notification if you are a party to a completed or planned qualifying acquisition that is not covered by mandatory notification and want to find out if the government is going to call it in.

Even if you do not notify an acquisition, if the government reasonably suspects it may give rise to a national security risk it may still be called in for a national security assessment. The government can assess acquisitions up to 5 years after they have taken place and up to 6 months after becoming aware of them if they have not been notified.

Submitting a notification form

There are 3 different forms that can be used to notify the government about an acquisition:

- mandatory notification form: as explained above, you are legally required to tell the government about notifiable acquisitions in 17 sensitive areas of the economy

- voluntary notification form: as explained above, you can submit a voluntary notification if you are a party to a completed or planned qualifying acquisition that is not covered by mandatory notification

- retrospective validation application form: as explained above, an acquisition is void if you complete a notifiable acquisition (which is subject to mandatory notification) without notifying and gaining approval from the government. You can apply for retrospective validation if you have completed a notifiable acquisition without notifying

You can submit a notification form using the National Security and Investment notification service.

There is further guidance on how to register for the online notification form service and complete notification forms.

After you’ve submitted a notification form

Accepting or rejecting a notification form

After you have submitted a notification form, the government will give you a case reference number and will confirm whether the form has been accepted or rejected as soon as is reasonably practicable after receiving it.

The notification form will only be accepted for consideration if it complies with the notification requirements and includes all the necessary information. Only then will the government process your notification form to the timescales set out in the NSI Act.

A notification form that is rejected will not progress to the next stage and will be returned with the reasons why it was not accepted. This applies to all types of notification form, whether mandatory, voluntary or retrospective.

The government may ask you to resubmit a notification form if more information is needed before it can be accepted.

Once a notification form has been accepted

The consideration of notifications is divided into 2 parts:

- the review period (applies to all notified acquisitions)

- the assessment period (applies only if an acquisition is ‘called in’)

The processes for review and, if required, assessment are the same for each type of notification, whether mandatory, voluntary or retrospective.

The review period and the assessment period each last up to 30 working days. The government may extend the assessment period by an additional period of 45 working days, subject to certain tests being met. Any further extension beyond those 45 working days must be with the written agreement of the acquirer (known as the ‘voluntary period’). In calculating these days, a working day is any day other than a Saturday, Sunday or a Bank Holiday anywhere in the UK.

Review period

The government will email you telling you it has accepted your notification form. The 30 working day period for the government’s review begins on the day this email is sent.

Within 30 working days of acceptance of the notification form

The government will either:

- clear the acquisition and tell you it can go ahead

- call in the acquisition for a full national security assessment

- require further information, which you should provide as soon as possible, to help complete the assessment (known as an ‘information notice’)

- require you or people involved in the acquisition to attend a meeting (known as an ‘attendance notice’)

We expect that most notifications will be cleared rather than called in, and you will be informed of the outcome of the government’s decision during the first 30 working day review period.

If the government wishes to call in the acquisition to investigate further, you will be informed by email on or before the final day of the review period.

Information or attendance notices issued during the review period do not change the 30 working day deadline. This is different from information notices and attendance notices issued during the assessment period, which have the legal effect of ‘stopping the clock’.

Assessment period

The government will tell you by email if it needs to carry out a full assessment of your acquisition for a national security risk. This is known as ‘call in’. The assessment will last up to 30 working days (subject to any extensions).

During this period, the government will carry out a detailed assessment of the potential national security risks and decide what, if any, action it considers necessary and proportionate to address any of these risks.

The government may extend the assessment period for an additional period of 45 working days (known as the ‘additional period’). Any further extension must be with the written agreement of the acquirer (known as the ‘voluntary period’).

What the government can ask you to do during the assessment period

During the 30-working day assessment period, the government can:

- put in place immediate and temporary controls to prevent you taking action that might undermine conditions the Secretary of State might seek to put in place (known as an ‘interim order’)

- require you to provide further information to help complete its assessment (known as an ‘information notice’)

- require you or people involved in the acquisition to attend a meeting (known as an ‘attendance notice’)

Information notices and attendance notices issued during the assessment period have the legal effect of ‘stopping the clock’. This is different from information notices and attendance notices issued during the review period. More detail is set out in the sections below.

Interim orders

An interim order may be issued at any time during the assessment period. Interim orders are intended to prevent you or other parties to the acquisition taking any steps which might undermine any conditions the Secretary of State may seek to put in place at the end of the assessment period through a final order.

Interim orders could include (but are not limited to) preventing the exchange of confidential information and access to sensitive sites or assets, pending the outcome of the assessment, and may include compliance monitoring requirements. Interim orders will be communicated to you by email.

The government may issue an interim order to any person (or to the holder of a position in the company), where provisions of the order are necessary and proportionate. Interim orders can apply to people outside the UK. You will be informed of the order’s details and rationale. The government will not routinely make interim orders public.

If you are required to comply with an interim order but wish to request that it be varied or revoked, the government must consider your request as soon as practicable after receiving it. The best way to make requests is by contacting the ISU by email.

Information notices

During the assessment period, the government may need more information. If this is the case, the government may issue an information notice, setting out the reason for requiring the information, how it should be provided, a time limit for providing the information and the potential consequences of not doing so. The ‘clock’ for assessing your acquisition stops until this information has been provided or the deadline for providing the information has passed. The clock will restart the day after the government has confirmed that either of these 2 things has happened.

Information notices can also be issued during the review period (the first 30 working days after your notification is accepted), but these will not result in a ‘clock stop’.

Attendance notices

The government may also need to hear from people involved in the acquisition to inform its decision making. This will be required through an attendance notice, setting out the time and place of the meeting, and the purpose of the meeting. This could include you (the representative of a party involved in the acquisition), people in specific positions in one of the companies involved (for example someone with technical knowledge of the business), or others as required.

You and/or others whose attendance is requested must attend this meeting. If the attendance notice is issued during the assessment period, the ‘clock’ for assessing your acquisition stops until the meeting has taken place and the required information has been provided or the deadline for complying with the attendance notice has passed. The clock will restart the day after the government has confirmed that either of these 2 things has happened.

Attendance notices can also be issued during the review period (the first 30 working days after your notification is accepted), but these will not result in a ‘clock stop’.

By the 30th working day of the assessment period

By the 30th working day, the government will inform you of one of the following:

- your acquisition is cleared and can carry on (the final notification)

- your acquisition can go ahead subject to certain conditions (the final order)

- your acquisition is blocked and cannot carry on (the final order)

- the assessment period needs to be extended for another 45 working days

A called in acquisition may be cleared by the government at any time during the assessment period. You will be informed by email.

If the government determines there are national security risks raised by your acquisition, representatives of the parties may be contacted at any stage during the assessment period to be informed of conditions the government may put in place through a final order. The purpose of these conditions is to mitigate risk (as determined by the government) and allow the acquisition to proceed.

You will be issued a ‘final order’ if the government imposes conditions on your acquisition, or if your acquisition is blocked. Relevant parties will be provided with information about the decision, including details of any conditions imposed and the consequence of any breach of these conditions, once a national security assessment has been concluded.

Before making a final order, the government must consider any representations made. Representations should be made to the government by contacting the ISU at investment.screening@beis.gov.uk.

Notices of final orders made by the government will be published on GOV.UK. The government will remove sensitive information.

If the assessment period is extended

The assessment period may be extended for another 45 working days where it is reasonably believed that a qualifying acquisition raises or would raise a national security risk and an additional period is required to further assess the acquisition. Any further extension beyond this must be with the written agreement of the acquirer (known as the ‘voluntary period’).

Carrying on an acquisition whilst review and assessment is ongoing

You can continue to progress an acquisition during the review and assessment periods up to the point of completion unless the government has told you not to through an interim order. Interim orders can only be issued during the assessment period, and may place immediate and temporary controls on the parties to prevent any action which could have the effect of undermining conditions the Secretary of State may seek to put in place through a final order.

In the case of mandatory notification, you must not complete the acquisition until you have received clearance from the government. If you do complete without clearance, the acquisition will be legally void.

In the case of a voluntary notification, you may choose to continue your acquisition (unless the government has told you not to do so through an interim order). However, if you choose to complete your acquisition before the government has made its decision, the acquisition can later be unwound if the government finds that there are national security concerns.

Confidentiality whilst review and assessment is ongoing

The government will not routinely make public that it has called in an acquisition for national security assessment or that it has issued an interim order and will inform you if it intends to do so.

Throughout the review and assessment periods, and in any interactions with the ISU, you should remain mindful of the other legislative obligations that you may be under. For example, if you are a relevant issuer, you will still need to comply with applicable transparency and disclosure obligations such as the obligation under the UK Market Abuse Regulation to disclose inside information to the public as soon as possible.

If your disclosure obligations give rise to any doubts or concerns about your ability to comply with any specific requirements raised during the review and assessment process, or as a result of interim or final orders you are subject to, you can contact the ISU by email at investment.screening@beis.gov.uk.

Find further information on the UK Market Abuse Regulation on the Financial Conduct Authority’s website.

After the assessment period

If no further action is being taken following the full national security assessment, you will be informed by the government that the acquisition has been cleared. That decision cannot be revisited. The only exception is if it is established that false or misleading information was provided in a notification form or in response to an information notice or attendance notice.

Where you are subject to interim orders or final orders, the government has a duty to keep these under review and to vary and/or revoke them, where appropriate. This would generally happen in discussion with the parties, who can also request that the order be reviewed.

Compliance and enforcement

Read guidance on how to comply with the National Security and Investment Act 2021 and what can be expected if you are subject to orders and notices.

How and when the government will publish information related to the NSI Act

There are no statutory requirements under the NSI Act for the government to publish information about individual acquisitions prior to a final order being made. The government is, however, required to publish notice of the fact that a final order has been made. This approach reflects the government’s intention to minimise the potential for the NSI system to create commercial distortions in the market.

The Act does not, however, preclude such announcements being made. There are a number of situations where this may be relevant, including:

- where a party is a public company and has existing statutory obligations to inform the market of price-sensitive information

- where a party wishes to communicate a decision publicly for business or reputational reasons

- where a party is seeking to raise external awareness of the government’s consideration of an acquisition

General practice

The government will not publish information regarding the receipt (or not) and the acceptance or rejection of individual notifications.

The government may choose to publish information regarding call-in notices or final notifications (clearances) following the review period – primarily either where the parties disclose such information, or the acquisition is otherwise in the public domain and the Business Secretary considers it is in the public interest to do so.

For acquisitions which are called in and subject to an interim order, the government will not publish information about the specific contents of any such order, but may choose to state that one has been made.

The government may choose to publish information regarding final notifications (clearances) following the assessment period – primarily either where the parties disclose such information, or the acquisition is otherwise in the public domain and the Business Secretary considers it is in the public interest to do so.

Process

Announcements will be made on GOV.UK

Where the government chooses to make a proactive announcement (that is, rather than responding to a prior disclosure by one or more of the parties), it will ordinarily seek to provide advance notices to the parties of the planned announcement and to make it when the relevant markets are closed.

Further guidance

For businesses seeking investment, considering potential security issues early in your investment planning can protect both your company and the UK’s national security. Read guidance on Informed Investment for practical advice on how to reduce potential risks associated with investment.

Contact the Investment Security Unit (ISU)

For general enquiries or informal discussion around future acquisitions or a specific notification, please contact the ISU at investment.screening@beis.gov.uk.

Last updated

-

Content relating to when to tell the government about an acquisition has been moved from the Market Guidance Notes July 2022 and incorporated into this guidance.

-

Content changed in the compliance and enforcement section

-

The NSI notification service will be unavailable from 4:00pm Sunday 20 March to 9:00am Monday 21 March 2022, due to routine maintenance work. If you have any notifications in progress they will not be affected.

-

The National Security and Investment notification service will not be available on Saturday 15 January 2022 between 8:00am and 9:00am while we undertake maintenance. If you have a notification in progress it won't be affected.

-

The National Security and Investment (NSI) Act came into force on 4 January 2022. The new rules have now started and the National Security and Investment notification service is open.

-

Guidance updated to provide further information on what to expect when an acquisition is being reviewed and assessed.

-

First published.